RETAIL SEAFOOD SALES IN THE UNITED STATES

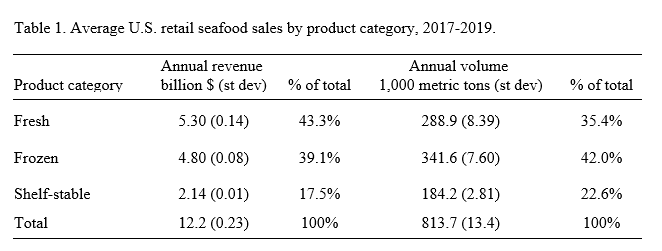

While a large number of studies have investigated seafood consumption in various markets, surprisingly little is known about the types of seafood sold in retail outlets in the United States. or their product forms. This is particularly true for what is generally regarded as the most valuable product form of seafood, fresh. In this paper we analyzed a unique dataset on retail in-store seafood sales that includes information about three main product forms (fresh, frozen and shelf-stable products). Fresh seafood is important, as it makes up 43% of sales revenue (Table 1). Moreover, some species are almost exclusively sold fresh, with trout and lobster as prime examples. Fresh also includes the greatest diversity of species, and as such, is the most likely product form for new producers to succeed. However, overall sales are dominated by a few species, with salmon and shrimp dominating the fresh (27%) and frozen categories (43%), respectively, and tuna dominating the shelf-stable category (75%). There are also a large number of species with mostly small market shares. There are few differences in regional sales patterns for the main species, with notable exceptions such as whitefish in New England and crawfish in Louisiana and Texas. The degree of urbanization and income level appear as important drivers for seafood sales.